Updated on Jul 25, 2021

Systematic Investment Plan (SIP)

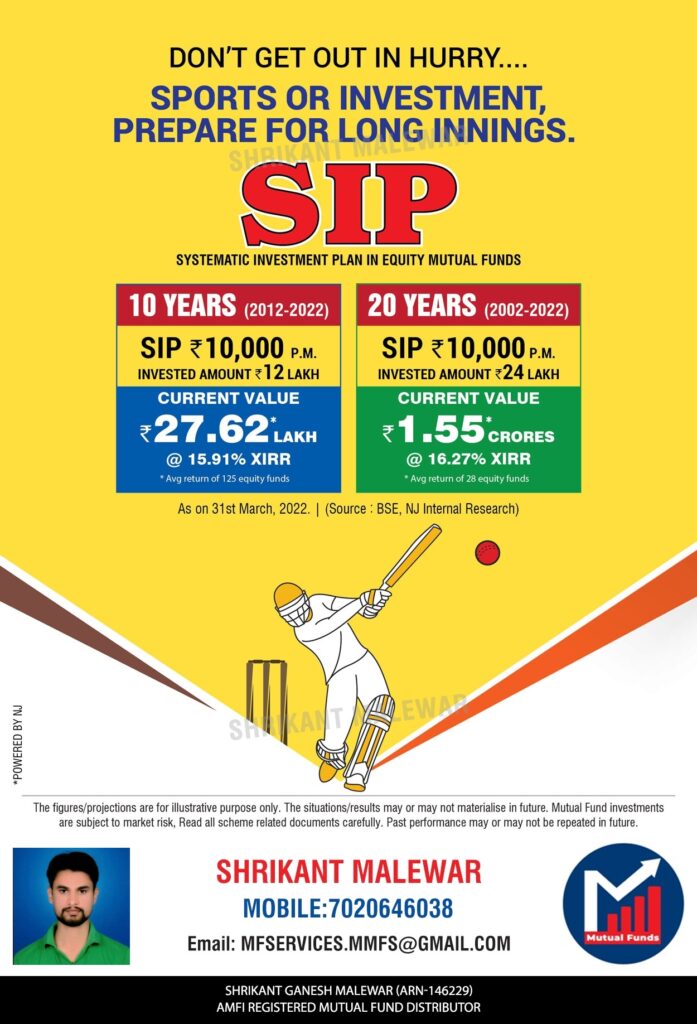

Systematic Investment Plan (SIP) is an investment plan (methodology) offered by Mutual Funds wherein one could invest a fixed amount in a mutual fund scheme periodically, at fixed intervals – say once a month, instead of making a lump-sum investment.

सिस्टमैटिक इन्वेस्टमेंट प्लान (एसआईपी) म्यूचुअल फंड द्वारा पेश की जाने वाली एक निवेश योजना (पद्धति) है, जिसमें कोई व्यक्ति एकमुश्त निवेश करने के बजाय समय-समय पर, निश्चित अंतराल पर – महीने में एक बार, एक निश्चित राशि का निवेश कर सकता है।

Click here to check your KYC status

The SIP installment amount could be as little as ₹500 per month. SIP is similar to a recurring deposit where you deposit a small /fixed amount every month.

SIP की किस्त राशि ₹500 प्रति माह जितनी कम हो सकती है। SIP एक आवर्ती जमा के समान है जहाँ आप हर महीने एक छोटी / निश्चित राशि जमा करते हैं।

SIP is a very convenient method of investing in mutual funds through standing instructions to debit your bank account every month, without the hassle of having to write out a cheque each time.

हर बार चेक लिखने की परेशानी के बिना, हर महीने अपने बैंक खाते को डेबिट करने के लिए स्थायी निर्देशों के माध्यम से म्यूचुअल फंड में निवेश करने का एक बहुत ही सुविधाजनक तरीका है।

SIP Become very Popular

SIP has been gaining popularity among Indian MF investors, as it helps in Rupee Cost Averaging and also in investing in a disciplined manner without worrying about market volatility and timing the market. Systematic Investment Plans offered by mutual funds are easily the best way to enter the world of investments over the long term.

एसआईपी भारतीय एमएफ निवेशकों के बीच लोकप्रियता हासिल कर रहा है, क्योंकि यह रुपये की औसत लागत में मदद करता है और बाजार की अस्थिरता और बाजार के समय की चिंता किए बिना अनुशासित तरीके से निवेश करने में भी मदद करता है। म्यूचुअल फंड द्वारा दी जाने वाली व्यवस्थित निवेश योजनाएं लंबी अवधि में निवेश की दुनिया में प्रवेश करने का सबसे अच्छा तरीका है।

Common sense suggests that “Buying low and selling high” is perhaps the best way to get good returns on your investments. But this is easier said than done, even for the most experienced investors. There are many factors at play when it comes to any market – debt or equity, and all of them are inextricably linked.

सामान्य ज्ञान बताता है कि “कम खरीदना और उच्च बेचना” शायद आपके निवेश पर अच्छा रिटर्न पाने का सबसे अच्छा तरीका है। लेकिन सबसे अनुभवी निवेशकों के लिए भी ऐसा करना आसान है। जब किसी बाजार की बात आती है तो कई कारक होते हैं – ऋण या इक्विटी, और ये सभी अटूट रूप से जुड़े हुए हैं।

Disciplining and Committing Investment

SIP is a simpler approach to long term investing is disciplining and committing to a fixed sum for a fixed period and sticking to this schedule regardless of the conditions of the market.

एसआईपी लंबी अवधि के निवेश के लिए एक सरल तरीका है, एक निश्चित अवधि के लिए अनुशासित और एक निश्चित राशि के लिए प्रतिबद्ध है और बाजार की स्थितियों की परवाह किए बिना इस शेड्यूल से चिपके रहना है।

Rupee cost averaging

Rupee cost averaging, as this practice is called, in a way ensures that you automatically buy more units when the NAV is low and fewer when the NAV is high…e.g., an SIP of ₹1000 gets you 50 units when the NAV is Rs. 20, but gets you 100 units when the NAV is Rs.10. The average cost for buying those 150 units would be Rs. 2000/150 units i.e. ₹ 13.33.

रुपये की औसत लागत, जैसा कि इस प्रथा को कहा जाता है, एक तरह से यह सुनिश्चित करती है कि एनएवी कम होने पर आप स्वचालित रूप से अधिक इकाइयाँ खरीदते हैं और एनएवी अधिक होने पर कम… जैसे, ₹1000 का एक एसआईपी आपको 50 यूनिट देता है जब एनएवी रु। 20, लेकिन एनएवी 10 रुपये होने पर आपको 100 यूनिट मिलती है। उन 150 इकाइयों को खरीदने की औसत लागत रु. 2000/150 यूनिट यानी ₹13.33।

However, please remember that the Rupee cost averaging does not assure profit, nor does it protect one against investment losses in declining markets. It merely ensures disciplined & regular investment in stock markets, which helps overcome the natural impulse to stop investing in a falling or a depressed market or investing a lot, when markets are buoyant and euphoric.

हालांकि, कृपया याद रखें कि रुपये की औसत लागत लाभ का आश्वासन नहीं देती है, न ही यह गिरावट वाले बाजारों में निवेश के नुकसान के खिलाफ किसी की रक्षा करती है। यह केवल शेयर बाजारों में अनुशासित और नियमित निवेश सुनिश्चित करता है, जो गिरते या उदास बाजार में निवेश को रोकने या बहुत अधिक निवेश करने के लिए प्राकृतिक आवेग को दूर करने में मदद करता है, जब बाजार में उत्साह और उत्साह होता है।

Visit our App store….हमारे ऐप स्टोर पर जाएं

The Power Of Compounding

There is a great advantage with long-term investments, namely, compounding which is considered one of the greatest mathematical discoveries.

लंबी अवधि के निवेश के साथ एक बड़ा फायदा है, अर्थात् कंपाउंडिंग जिसे सबसे बड़ी गणितीय खोज में से एक माना जाता है।

To put it in simple words, compounding is when the interest (or income) you earn is reinvested in the original corpus and the accumulated corpus continues to earn (& grow). Every time this happens, your investment keeps growing, paving the way for a systematic accumulation of money, multiplying over time.

इसे सरल शब्दों में कहें तो चक्रवृद्धि तब होती है जब आप जो ब्याज (या आय) अर्जित करते हैं, उसे मूल कोष में पुनर्निवेशित किया जाता है और संचित कोष अर्जित करना (और बढ़ना) जारी रहता है। हर बार ऐसा होने पर, आपका निवेश बढ़ता रहता है, धन के व्यवस्थित संचय का मार्ग प्रशस्त करता है, समय के साथ बढ़ता जाता है।

To illustrate, a small amount of ₹1000 invested every month at an interest rate of 8% for 25 years would give you ₹ 9.57 Lakh! That means your investment of just 3 Lakh would have grown three times over!

उदाहरण के लिए, 25 वर्षों के लिए 8% की ब्याज दर पर हर महीने निवेश की गई ₹1000 की एक छोटी राशि आपको ₹ 9.57 लाख देगी! इसका मतलब है कि आपका सिर्फ ₹3 लाख का निवेश तीन गुना बढ़ गया होगा!

Starting Early Pays Well

To get the best out of your investments, it is very important to invest for the long-term, which means that you should start investing early, in order to maximize the end returns.

अपने निवेश से सर्वोत्तम लाभ प्राप्त करने के लिए, लंबी अवधि के लिए निवेश करना बहुत महत्वपूर्ण है, जिसका अर्थ है कि आपको अंतिम रिटर्न को अधिकतम करने के लिए जल्दी निवेश करना शुरू कर देना चाहिए।

Let’s understand this better through an illustration

Let’s assume that two friends, both aged 25, decide to invest ₹ 2000 every month for a period of 5 years and earn 8% p.a. on a monthly compounding basis. The only difference is that while one starts investing promptly at the age of 25 itself, the other starts investing 10 years later at the age of 35 years. Both decide to hold on to their investments till they turn 60. So while both of them would accumulate a principal investment of ₹1.2 Lakh over a period of 5 years, the investment of the person who started early at the age of 25 appreciates to over 14 Lakh, and the investment of the second person who started later grows to only about ₹ 6 Lakh.

मान लेते हैं कि दो दोस्त, दोनों की उम्र 25, 5 साल की अवधि के लिए हर महीने ₹2000 का निवेश करने का फैसला करते हैं और 8% प्रति वर्ष कमाते हैं। मासिक चक्रवृद्धि आधार पर। फर्क सिर्फ इतना है कि एक जहां 25 साल की उम्र में तुरंत निवेश करना शुरू कर देता है, वहीं दूसरा 10 साल बाद 35 साल की उम्र में निवेश करना शुरू कर देता है। दोनों 60 साल की उम्र तक अपने निवेश को बनाए रखने का फैसला करते हैं। इसलिए जब दोनों 5 साल की अवधि में ₹ 1.2 लाख का मूल निवेश जमा करेंगे, तो 25 साल की उम्र में शुरू होने वाले व्यक्ति का निवेश ₹ से अधिक की सराहना करता है। 14 लाख, बाद में शुरू करने वाले दूसरे व्यक्ति का निवेश केवल ₹6 लाख तक ही बढ़ता है।

Thus, you can clearly see the difference between the two and the clear advantage of investing early. So go ahead. Start investing through SIP today itself.

इस प्रकार, आप स्पष्ट रूप से दोनों के बीच अंतर और जल्दी निवेश करने का स्पष्ट लाभ देख सकते हैं। तो आगे बढ़ो। आज ही SIP के जरिए निवेश करना शुरू करें।

Investor Awareness Program निवेशक जागरूकता कार्यक्रम

- Be Intelligent Investor

- ELSS(Tax Saving)

- Equity Funds

- Events and Announcements

- Investor Awareness

- Market Updates

- mf_news

- Minor Investment

- NFO

- NPS

- Retirement_Plan

- SIP

- Type of Investment